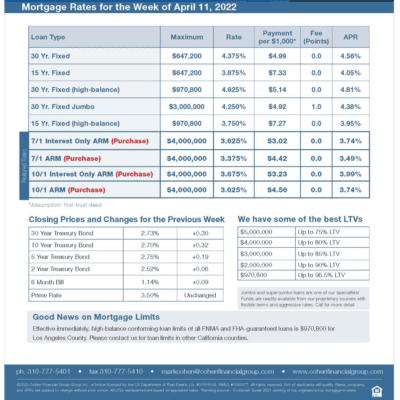

New Fed Plans Drive Interest Rates Higher

Investors were focused on Fed policy last week. The Fed plans to reduce its massive portfolio of bonds more quickly than expected, which was negative for mortgage rates, and they rose to the highest levels since late 2018.

To review, the Fed loosens monetary policy to boost the economy during periods of weakness, such as after the start of the pandemic. By contrast, when the economy exceeds a certain capacity, the demand for goods and services becomes so strong that prices must rise to balance supply and demand, eventually forcing the Fed to tighten.

The challenge is to implement the optimal level of tightening which will restrain economic growth just the right amount to bring down inflation without causing an undesirable recession.

Adjusting the federal funds rate and the size of the bond portfolio are the two primary tools used by the Fed to achieve its goals. Three weeks ago, the Fed provided fairly precise guidance on the projected pace of rate hikes. Last week, the plans for the bond portfolio were revealed. In short, officials expressed more concern about upside risks to inflation than downside risks to economic growth.

The minutes from the March 16 Fed meeting released on Wednesday indicated that the Fed plans to allow its holdings of Treasuries and mortgage-backed securities (MBS) to decrease by up to $95 billion per month, which was higher than anticipated, likely beginning in May. The split will be $60 billion in Treasuries and $35 billion in MBS, phased in over three months. While these quantities are quite large on a historical basis, they must be viewed in the context of nine trillion dollars of total bond holdings, double the levels held prior to the pandemic. Since mortgage rates are largely based on MBS prices, the reduced outlook for Fed demand for MBS caused rates to move higher.

Service Sector Expanding

The most significant economic indicator released this week from the Institute of Supply Management (ISM) remained at a high level by historical standards. The national service sector index for March rose to 58.3. Levels above 50 indicate that the sector is expanding, and readings above 60 are rare. Investors are watching to see how much consumer spending is shifting from goods to services.

Major Economic News Due This Week

Looking ahead, investors will continue to closely follow news on Ukraine and will look for additional Fed guidance on the pace of future rate hikes and balance sheet reduction. Beyond that, the Consumer Price Index (CPI) will be released tomorrow. CPI is a widely followed monthly inflation indicator that looks at the price changes for a broad range of goods and services. Retail Sales will come out on Thursday. Since consumer spending accounts for over two-thirds of U.S. economic activity, the retail sales data is a key indicator of growth.

mortgage rates week of 4-11-2022