Global Bank Monetary Tightening

Last week, investors raised their outlook for monetary policy tightening by global central banks, mostly due to an unexpected change from the Bank of Japan. As a result, mortgage rates ended the week higher.

Lower Inflation in Japan

Japan has a more insulated economy than the US or European countries, and inflation has remained much lower there. The Bank of Japan (BOJ) also has conducted monetary policy differently than the US Fed or the European Central Bank in a couple of significant ways. First, it has not raised rates this year to fight inflation. In addition, it has held Japanese bond yields in a very narrow range by buying or selling bonds to offset further movement when the limits of the range are reached.

Global Yields Rise

On last Tuesday, investors were caught by surprise when the BOJ announced that it will allow the 10-year Japanese bond to trade in a wider range. While the BOJ simply said that this was to help financial markets function more smoothly, investors considered this to be potentially the first step on the path toward tighter monetary policy. The possibility of reduced future demand for bonds from the BOJ caused global yields to rise, including US mortgage rates.

PCE Remains Above Fed Target Level

The PCE price index is the inflation indicator favored by the Fed because it adjusts for changes in consumer preferences over time. In November, core PCE was up 4.7% from a year ago, matching expectations, and down from an annual rate of 5.0% last month. However, this remains far above the Fed’s stated target level of 2.0%. How quickly monetary policy tightening will bring down inflation and close this gap has enormous implications for financial markets.

Home Sales Fall for 10th Month

Hurt by higher mortgage rates, sales of existing homes fell for the tenth straight month in November to the lowest level since 2010 and were 35% lower than last year at this time. Inventory levels were a little higher than a year ago, but they remain at just a 3.3-month supply nationally, far below the 6-month supply typical in a balanced market. While the median existing-home price of $370,700 was 4% higher than a year ago, this was down from a record high of $413,800 in June.

Mortgage Rates Declined in November

Additional home inventory has been badly needed for quite a while, but higher prices for land, materials, and skilled labor continued to hold back builders. In November, single-family housing starts were down 4% from October to the lowest level since May 2020. Single-family building permits, a leading indicator, fell 7% from October and were 30% lower than a year ago. In addition, a survey of home builder sentiment from the NAHB declined for the twelfth straight month to 31, the lowest reading since 2012. A level below 50 is considered negative. While there were few bright spots in the latest housing data, mortgage rates have declined substantially since early November, so these figures may improve next month.

Major Economic News Due This Week

Investors will continue looking for guidance on the magnitude of future rate hikes and bond portfolio reduction. The final week of the year will be a very light one for economic data. Next month, the ISM national manufacturing index will be released on January 4 and the ISM national services index on January 6. The key Employment report also will come out on January 6.

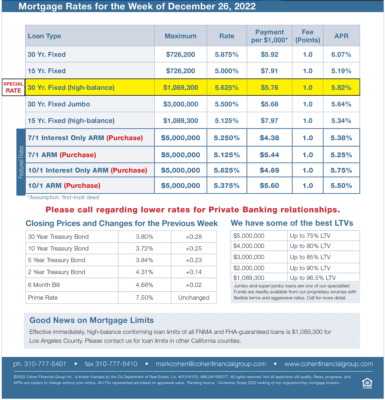

Mortgage Rates for the week of 12-26-2022