Central Banks – Raising Rates

Keeping in mind that slower economic growth, lower inflation are favorable for bonds, a wide range of major economic news last week was mostly positive for mortgage rates. Both the US Fed and European Central Bank announced the expected rate hikes last week and emphasized the need for additional tightening, perhaps even more than investors had anticipated. In addition, the latest inflation data was lower than expected and consumer spending came in below the forecasts. As a result, mortgage rates ended the last week lower.

Fed and ECB Raise Rates to Fight Inflation

At the meeting on last Wednesday, the Fed raised the federal funds rate by 50 basis points to a target range of 4.25% – 4.50%, the highest level since December 2007. Investors immediately focused on the latest projections from officials for the terminal (peak) rate which increased to 5.10%, above the investor outlook of around 4.90% prior to the meeting. During his press conference, Fed Chair Powell remained firmly committed to fighting inflation but appeared to leave the door open if inflation were to decline unexpectedly quickly. While noting that it will take “substantially more evidence,” Powell hinted that the Fed would be willing to scale back its monetary policy tightening if the data convincingly indicates that inflation is on a “sustained downward path.” The European Central Bank (ECB) also raised benchmark rates by 50 basis points and delivered a similar message about doing whatever it takes to bring down inflation.

Consumer Price Index Meets Fed Target Levels

The Consumer Price Index (CPI) is a closely watched inflation indicator that looks at price changes for a broad range of goods and services. Core CPI excludes the volatile food and energy components and provides a clearer picture of the longer-term inflation trend. Core CPI in November was up 6.0% from a year ago, below the consensus forecast and down from 6.3% last month. Bigger picture, however, inflation remains far above the readings around 2.0% seen early in 2021, which is the stated target level of the Fed.

Consumer Spending Triggering Concern

Consumer spending accounts for over two-thirds of US economic activity, making it an important indicator of the health of the economy. In November, retail sales fell 0.6% from October, well below the consensus forecast for a decline of just 0.3%. The pullback was widespread, and particular weakness was seen in furniture stores, building materials, and auto dealers. This report increased investor concerns about a slowdown in shopping due to higher prices and economic uncertainty heading into the crucial holiday season.

Inflation Rate Dropping

From the point of view of a bond investor, the events this week painted a pleasing picture. The annual inflation rate has been dropping more quickly than expected over the last couple of months. In addition, the significant decline in consumer spending suggests slower economic growth, which would reduce future inflationary pressures. Finally, central bank officials remain firmly committed to additional monetary policy tightening to further restrain the economy and bring down inflation.

Major Economic News Due This Week

Investors will be looking for guidance on the magnitude of future rate hikes and bond portfolio reduction. Housing Starts will be released on Tuesday. Existing Home Sales will come out on Wednesday and New Home Sales on Friday. The core PCE price index, the inflation indicator favored by the Fed, also will be released on Friday.

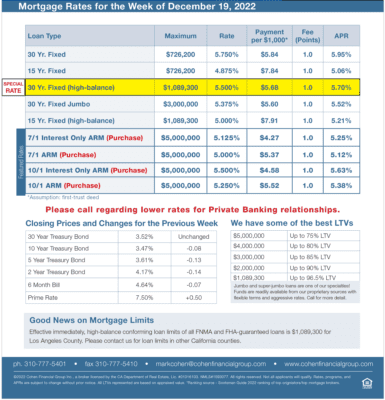

Mortgage Rates for the week of 12-19-2022